With the volatility in global equity markets this year, it may be comforting for investors to focus solely on US markets. However, it may be riskier to be geographically myopic now.

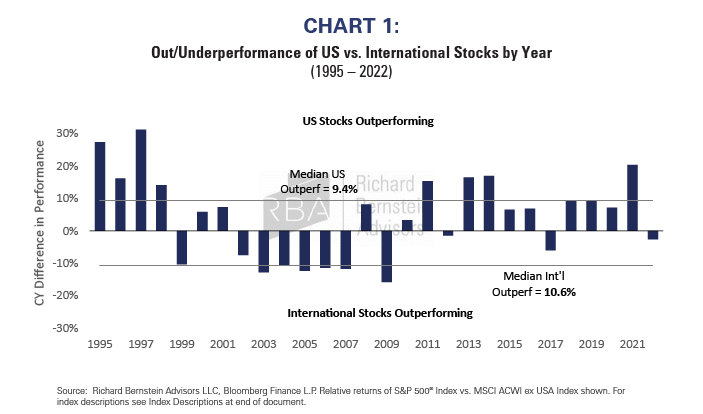

Global markets tend to go through cycles when US stocks or international stocks outperform, and investors’ decisions how to position across these markets can have significant implications for performance. In a typical year, returns on US and international stocks differ by more than 10 percentage points (Chart 1).

Two of the key drivers behind these meaningful return differences are sector exposures and country-specific factors.

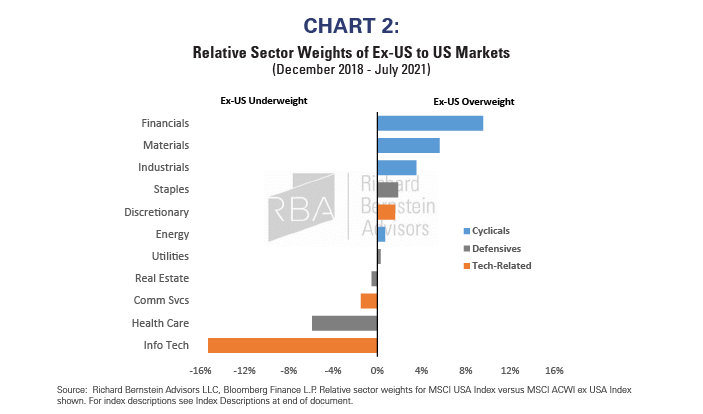

International markets are less exposed to tech stocks

The US market is highly concentrated in technology and other expensive growth stocks, with tech-related sectors making up nearly half (43%). Most non-US markets are much less exposed, and ex-US has a third less exposure overall than the US (Chart 2). While tech-related sectors performed well during periods of lower interest rates, high liquidity, and strong growth, today’s macro fundamentals are the opposite. So, international markets currently look attractive for their lower exposure to these vulnerable sectors.

Chart 2. Relative Sector Weights of Ex-US to US Markets

Source: Richard Bernstein Advisors LLC, Bloomberg Finance L.P. Relative sector weights for MSCI USA Index versus MSCI ACWI ex USA Index shown. For index descriptions see Index Descriptions at end of document.

Last cycle’s leadership is rarely the next cycle’s leadership. If we are correct that inflation and interest rates will remain higher for longer, international markets’ sector exposure might boost performance. Materials and Energy stocks likely benefit from higher commodity price inflation. Financials, especially European ones, may see improved profitability after having been hamstrung for years by low and negative interest rates. Although concerns about banks have recently surfaced globally, policymakers seem committed to preventing banks’ future liquidity issues turning into solvency concerns.

Returns across regions are increasingly different

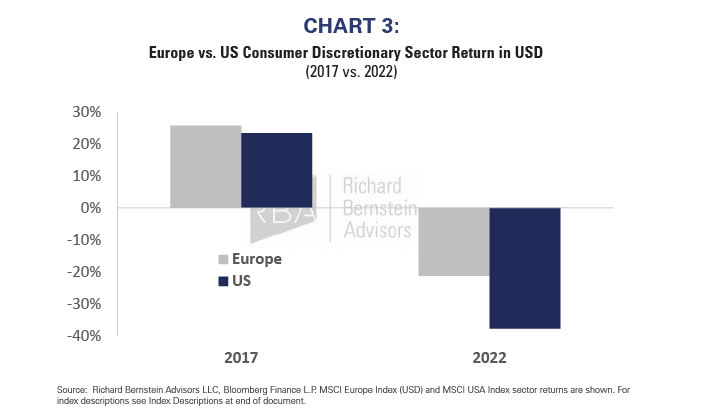

If differences in US and international market returns were only driven by sectors, there would be little need to invest globally; one could simply invest in US sectors. Many regional and country equity markets have moved in lockstep for much of the last two decades, helped in part by increased globalization. However, global equity markets may be going through a sea change.

In 2017, the last year before global uncertainty began to flare, it didn’t matter much where someone invested in consumer discretionary stocks, but just simply that one owned them. US discretionary stocks were up 23% while those in Europe returned 26% (in USD). But recently, sector returns have been less homogenous. Last year, consumer discretionary stocks were down -38% in the US while only down -21% in Europe (Chart 3).

Chart 3. Europe vs. US Consumer Discretionary Sector Return in USD, 2017 vs. 2022

Source: Richard Bernstein Advisors LLC, Bloomberg Finance L.P. MSCI Europe Index (USD) and MSCI USA Index sector returns are shown. For index descriptions see Index Descriptions at end of document.

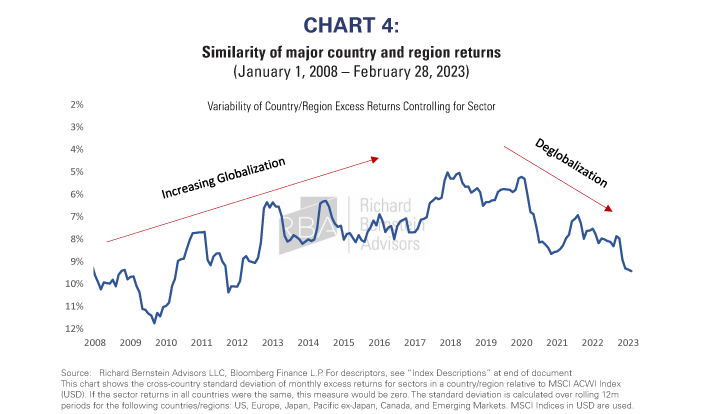

This variability in sector returns across regions has been broadly increasing in recent years (Chart 4). Retreating globalization as policymakers emphasize domestic activity and growth cycles’ decoupling as countries exited the pandemic at different times may explain part of the story. Increasing geopolitical turmoil and the Russia-Ukraine war may also contribute to less similar country returns.

Chart 4. Similarity of major country and region returns[1]

Source: Richard Bernstein Advisors LLC, Bloomberg Finance L.P.

It will be increasingly important to correctly allocate across countries (in addition to sectors) if this trend continues. While US stocks have led global markets over the last decade, it may now be wise for investors to look for opportunities internationally. Regions with more supportive liquidity and weaker investor sentiment may be some such opportunities abroad.

US liquidity is retreating more quickly than elsewhere

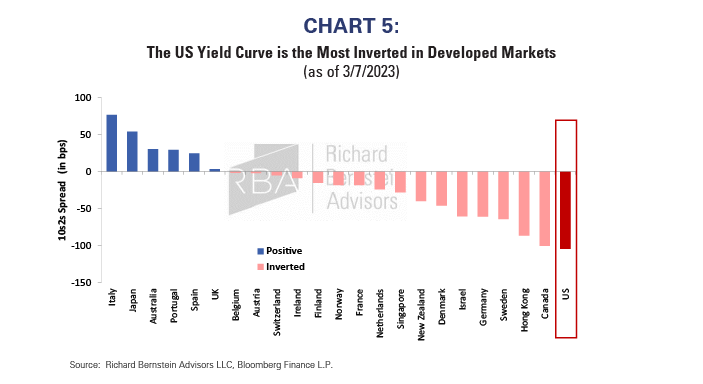

The Federal Reserve has been the most aggressive central bank in raising rates among developed markets and yet it is still struggling to rein in inflation. A central bank’s policy stance and outlook can be assessed through the slope of the country’s yield curve. Inverted curves tend to indicate monetary policy is restrictive and tightening, and currently 17 of the 23 developed market countries have inverted yield curves. The US is the most inverted of them all at -104bps (Chart 5).

Chart 5. The US Yield Curve is the Most Inverted in Developed Markets[2]

Source: Richard Bernstein Advisors LLC, Bloomberg Finance L.P.

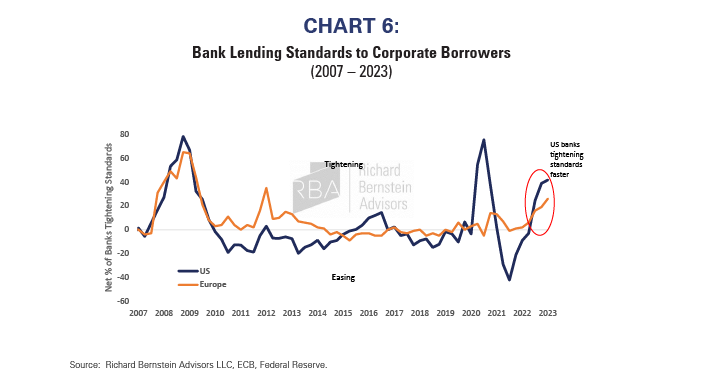

Bank lending standards paint a similar picture. US banks are rapidly tightening access to credit, outpacing banks in other major regions (Chart 6). In the wake of the recent US bank failures, it appears likely that regional and smaller banks will increasingly tighten standards even further. This means US companies may face higher borrowing costs and have less access to credit, which would weigh on future growth and the prospects for US stocks.

European banks were more restrictive than their US counterparts for nearly 5 years following the Global Financial Crisis, which may have contributed to Europe’s slower recovery. But recently, Europe’s banks have been slower to restrict lending than their US counterparts, which may benefit European companies relative to those in the US.

Chart 6. Bank Lending Standards to Corporate Borrowers

Source: Richard Bernstein Advisors LLC, ECB, Federal Reserve.

Larger valuation cushion in international markets

International markets trade at a huge discount to the US, reflecting investors’ more negative sentiment toward them. Given the war in Ukraine, the property malaise and rising Sino-US geopolitical tensions in China, and political uncertainty in EM, there are reasonable concerns about investing internationally. But, while ex-US markets’ cheaper valuations price in these risks, US markets still appear stubbornly ignorant of risks within the US.

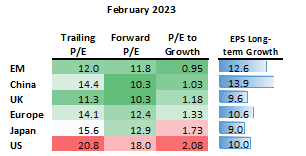

Admittedly, cheap markets aren’t always attractive investments. Those with deteriorating earnings may appear cheap, only to have fundamentals converge downward to price. While we want to avoid these “value traps”, growth expectations for international markets are largely similar to or stronger than those for the US (Chart 7).

Yet, investors still appear fixated on the drivers of growth over the last decade rather than on the drivers of growth in the coming years. If analysts’ estimates for long-term EPS growth end up correct, investors in US stocks could end up paying nearly twice as much for less growth than in many ex-US markets (Chart 7). While valuation is not an effective tactical timing indicator, it provides important insight into the balance of risk and reward within markets and has enormous importance for long-term returns.

Chart 7. Valuation Measures of US vs. Select Major International Markets

Source: Richard Bernstein Advisors LLC, Bloomberg Finance L.P. MSCI indices are used. For index descriptions see Index Descriptions at end of document.

The rising tide that drove stellar US performance last decade may now be going out. International markets’ cheaper valuations and relatively more accommodative liquidity suggests that investors with US-heavy portfolios may want to consider diversifying with opportunities outside the US.

For more news, information, and analysis, visit the ETF Strategist Channel.

INDEX DESCRIPTIONS:

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results.

Each index reflects an unmanaged universe of securities without any deduction for advisory fees or other expenses that would reduce actual returns, as well as the reinvestment of all income and dividends. An actual investment in the securities included in the index would require an investor to incur transaction costs, which would lower the performance results. Indices are not actively managed and investors cannot invest directly in the indices.

Sector/Industries: Sector/industry references in this report are in accordance with the Global Industry Classification Standard (GICS®) developed by MSCI Barra and Standard & Poor’s.

Country performance: MSCI All Country Indices. The MSCI All Country indices are a set of free-float-adjusted, market-capitalization-weighted indices designed to measure the equity-market performance of each country included in the MSCI All Country World Index.

S&P 500®: S&P 500® Index: The S&P 500® Index is an unmanaged, capitalization-weighted index designed to measure the performance of the broad US economy through changes in the aggregate market value of 500 stocks representing all major industries.

MSCI ACWI ex USA®: MSCI All Country World Index excluding USA. The MSCI ACWI® ex USA is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of global developed and emerging markets excluding the United States.

MSCI ACWI®: MSCI All Country World Index. The MSCI ACWI® Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of global developed and emerging markets.

MSCI Europe: MSCI Europe Index: The MSCI Europe Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of Europe developed markets.

MSCI USA: MSCI USA Index: The MSCI USA Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of the United States.

MSCI UK: MSCI United Kingdom (UK) Index: The MSCI United Kingdom Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of the United Kingdom.

MSCI Japan: MSCI Japan Index: The MSCI Japan Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of Japan.

MSCI Emerging Markets: MSCI Emerging Markets Index: The MSCI Emerging Markets Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of global emerging markets.

MSCI China: MSCI China Index: The MSCI China Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of China.

[1] This chart shows the cross-country standard deviation of monthly excess returns for sectors in a country/region relative to MSCI ACWI Index (USD). If the sector returns in all countries were the same, this measure would be zero. The standard deviation is calculated over rolling 12m periods for the following countries/regions: US, Europe, Japan, Pacific ex-Japan, Canada, and Emerging Markets. MSCI Indices in USD are used.

[2] Source: RBA LLC, Bloomberg, L.P. Data are as of 3/7/2023.

Read more on ETFtrends.com.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.