Tamil Nadu needs to sustain an annual growth rate of over 12 per cent to achieve its ambitious goal of becoming a $1-trillion economy by 2030, according to the State’s first Economic Survey. Tamil Nadu’s Gross State Domestic Product (GSDP) stood at ₹27.22 lakh crore in 2023-24, with a real growth rate of 8.23 per cent and while the current momentum is strong, a significant acceleration in economic expansion is essential to meet the $1-trillion target within the next six years, the survey said.

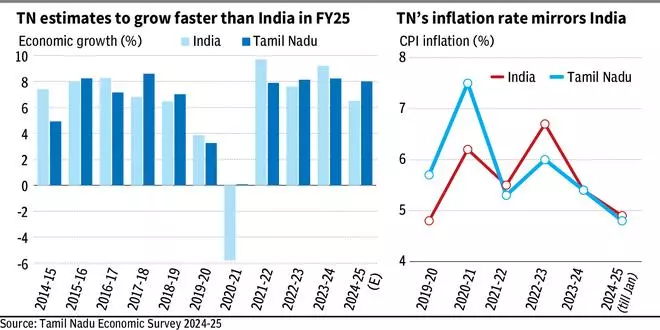

“India’s economy recorded 7.61 per cent growth in 2022-23, 9.19 per cent in 2023-24 and 6.48 per cent in 2024-25. Building on a strong foundation of inclusive policies, Tamil Nadu has demonstrated a remarkable economic resilience, consistently achieving growth rates of 8 per cent or more since 2021-22. The State is expected to maintain a growth rate above 8 per cent in 2024-25,” it added.

For the short-term, the Survey estimates the State will maintain a real growth rate of ~9 per cent with an inflation rate of around 5 per cent as largescale infrastructure projects, industrial growth, and foreign investments spur economic activity. “Over the medium term, this growth rate may moderate to 8 per cent with a 4 per cent inflation,” it added.

In 2023-24, the services or tertiary sector contributed 53.63 per cent of the State’s Gross State Value Added (GSVA)) in 2023-24, followed by the secondary sector (33.37 per cent) and the primary sector (13 per cent). Talking about inflation in the State, the Survey noted that India’s retail (CPI) inflation was 5.4 per cent in 2023-24 and 4.9 per cent in 2024-25 (till Jan 2025), and Tamil Nadu too mirrors the same at 5.4 per cent in 2023-24 and down to 4.8 per cent in 2024-25 (till January 2025).

Concerted effort

Speaking to media persons about Tamil Nadu’s first Economic Survey, J Jeyaranjan, Executive Vice-Chairman of the State Planning Commission, said that the survey could not make growth projections for future years due to challenges such as climate change and technological disruptions. As a major exporter of automobiles, textiles, leather and IT services, the economy is responsive to global market trends and is closely connected with global economic fluctuations, he added.

The survey acknowledged that sustaining 12 per cent growth will require a concerted effort, including sustained public and private investments, enhanced ease of doing business and inclusive policies. Encouraging investments, innovation and exports will help ensure steady economic growth and resilience, the survey pointed out.

Despite a declining share in the State’s GSVA, the survey pegs agriculture as a vital source of employment, necessitating continued support and modernisation. To sustain growth in agriculture, Tamil Nadu is prioritising technology adoption, irrigation improvements, and diversification into allied sectors such as livestock, inland fishing and food processing, the survey noted.

Industrial sector

Tamil Nadu’s industrial sector remains deeply integrated with the global economy, leveraging its strong foundations in automobile manufacturing, machinery, light engineering and textiles, both in large-scale industries and MSMEs. With a robust manufacturing ecosystem and export-oriented industries, the State continues to be one of India’s top industrial hubs. However, adapting to global shifts requires innovative strategies, including industrial housing, entrepreneurship programmes and advanced manufacturing facilities.

Tamil Nadu’s services sector remains a key economic driver, with strong foundations in IT & ITeS, finance, healthcare, education and tourism. The State has emerged as a hub for Global Capability Centres (GCCs), offering high-value finance, R&D and operational services for global firms. As AI-driven changes reshape the IT industry, workforce re-skilling will be crucial to maintaining Tamil Nadu’s competitive edge.

To sustain its competitive advantage, Tamil Nadu must focus on enhancing digital infrastructure, strengthening urban mobility and promoting skill development in emerging fields such as AI, fintech and cloud computing. Regulatory improvements and ease-of-doing-business reforms will also be essential in attracting new investments in the services sector, said the survey.